Traditional banks still take 3 to 5 days to send money across borders. Fees? Around 6.4% on average. And you never really know what exchange rate you’re getting until it’s too late. Meanwhile, a new system is quietly replacing it-using crypto, but not the kind you gamble with. It’s called stablecoin payments, and it’s already moving over $19 trillion in cross-border transactions annually. That’s 12.7% of the global total. Here’s how it works, where it beats banks, and where it still falls short.

How stablecoin payments actually work (no jargon)

Forget Bitcoin. The real players here are USDT, USDC, and EURAU-stablecoins tied to real currencies like the dollar or euro. They don’t swing in price. That’s key.

Here’s the simple flow: You send euros from Germany to Mexico. Instead of waiting for SWIFT, your payment platform instantly converts euros into USDT. That USDT zips across the blockchain in under 10 seconds. In Mexico, it’s instantly turned back into pesos and deposited into the recipient’s bank account. Total time? 5 to 10 minutes. Cost? 0.5% to 1.2%. Compare that to traditional banks, which charge 4-8% and take days.

This is called the stablecoin sandwich. Fiat → stablecoin → fiat. No middlemen. No holding tanks. Just code.

Why it’s faster than banks

Banks rely on a chain of correspondent accounts. If you’re sending money from Nigeria to Brazil, your bank has to talk to another bank, which talks to another, and so on. Each step adds delay, fees, and opacity.

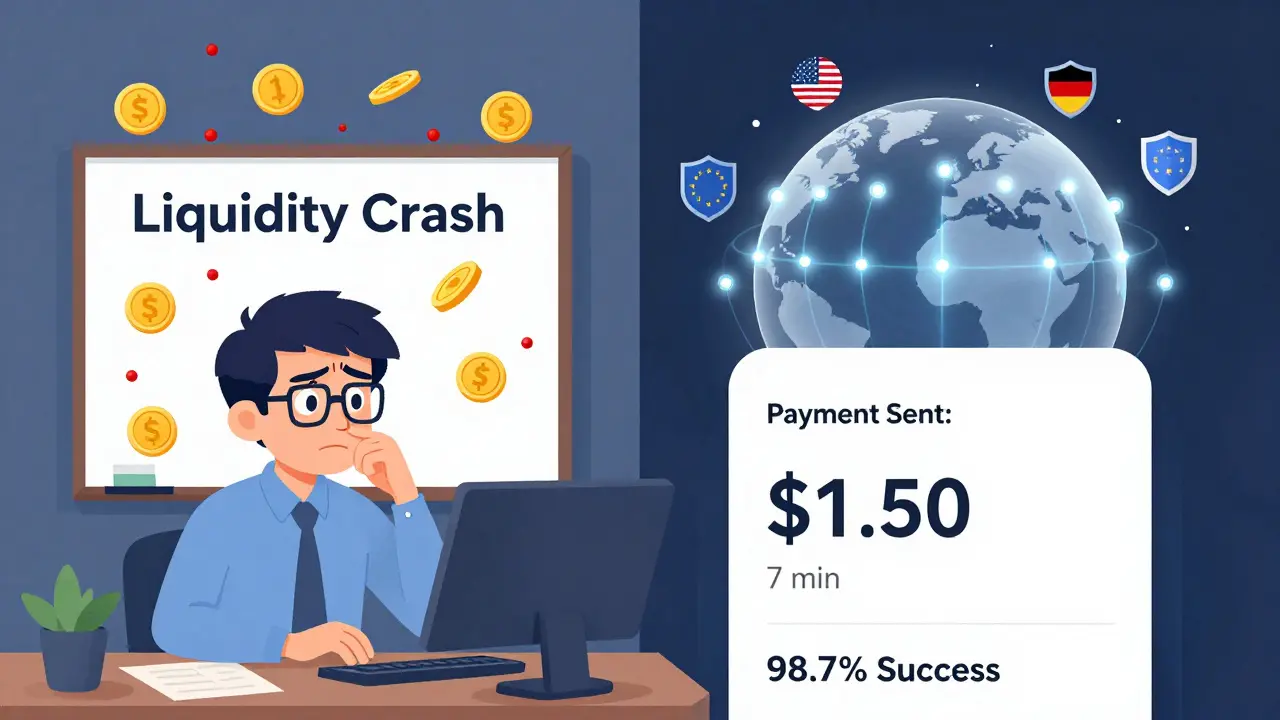

Blockchain cuts that out. Transactions settle directly between two points. Ethereum’s Layer 2s, Solana, and Polygon handle these transfers with finality in 2.5 to 15 seconds. That’s not theoretical. In March 2025, BVNK’s system processed 427,000 cross-border payments with an average settlement time of 7.3 minutes. Success rate? 98.7%. Traditional SWIFT? 63.2%.

And it’s not just speed. The exchange rate is locked in upfront. No surprise markup. No hidden fees. You see the exact amount the recipient will get before you hit send.

Where it’s making the biggest difference

It’s not rich countries where this shines-it’s emerging markets.

In Mexico, 22% of all inbound remittances now come through USDT, according to the Bank of Mexico. Workers in the U.S. send money home faster, cheaper, and with more certainty. In India, businesses using USDC for payments report 2.3% savings on FX costs compared to traditional wire transfers.

Why? Because traditional banking infrastructure is weak or expensive there. In Nigeria, a bank transfer can take a week. With stablecoins? If liquidity is available, it’s done before lunch.

Even PayPal, a company built on traditional finance, now offers crypto payment integration to 12,000+ merchants. They reported a 34% drop in cross-border processing costs. That’s not a pilot. That’s scale.

The hidden cost: Liquidity and regulation

It’s not magic. It needs infrastructure.

For a payment corridor like USD to MXN to work, someone has to hold pesos in Mexico and dollars in the U.S. That’s liquidity. And it costs money. Successful providers need at least $5 million per corridor in reserve. If liquidity dries up-say, during a crypto crash-payments stall.

That’s what happened in March 2024. When Bitcoin dropped 40% in 48 hours, some off-ramp providers couldn’t convert USDT fast enough. Settlement times jumped from 10 minutes to 30 minutes. A Brazilian fintech lost $1.2 million because its liquidity partner went insolvent.

Then there’s regulation. There are 37 different regulatory frameworks for stablecoins worldwide. Germany approved EURAU in January 2025. The U.S. passed the GENIUS Act in December 2024. The EU’s MiCA rules are live. But in Nigeria, Indonesia, or Argentina? Rules are unclear-or banned outright.

As a result, 70% of all stablecoin volume flows through just 15 corridors. The rest? Dead ends.

Who’s winning? Who’s losing?

Here’s the breakdown as of mid-2025:

| Provider | Market Share | Primary Blockchain | Key Use Case |

|---|---|---|---|

| Ripple (XRP) | 38% | XRP Ledger | Enterprise corporate payments |

| Circle (USDC) | 32% | Ethereum, Solana | Fintechs, remittance apps |

| Tether (USDT) | 25% | Omni, Ethereum, Tron | Emerging markets, peer-to-peer |

| Other stablecoins | 5% | Multiple | Regional, niche |

Traditional players like PayPal, Mastercard, and Visa now handle 58% of enterprise adoption-not because they’re crypto-native, but because they’re integrating stablecoins into their existing systems. They’re not replacing banks. They’re upgrading them.

What you lose going crypto

Stablecoins beat banks on speed and cost. But they don’t beat them on trust.

Traditional banks offer FDIC insurance. If your bank fails, you get your money back. With crypto? No such guarantee. If the off-ramp provider goes under? You’re out.

Also, tax authorities don’t always know what to do with crypto payments. Users on Reddit report being audited because their “crypto deposit” looked like income. Banks? You get a 1099. Crypto? You get a headache.

And while most transactions settle in minutes, you still need a wallet, a private key, and basic blockchain literacy. If your grandmother in rural Peru doesn’t have a smartphone or understand QR codes? This doesn’t help her.

Can it replace banks entirely?

No. Not yet.

But it’s replacing parts of them. Specifically, the slow, expensive, opaque middle layer.

By 2027, McKinsey predicts stablecoins will handle 20-25% of global cross-border payments. That’s not replacement. That’s transformation. Banks aren’t disappearing-they’re becoming interfaces. Your bank app might soon say: “Send pesos to Mexico? We’ll use USDT. It’ll cost $1.50 and arrive in 8 minutes.”

The real competition isn’t crypto vs. banks. It’s efficient vs. obsolete.

How to get started (if you’re a business)

If you’re a small business sending money internationally:

- Choose a regulated provider like BVNK, OpenPayd, or Coinbase Commerce. Avoid unlicensed platforms.

- Ensure they have liquidity in your destination country. Ask: “Do you have pesos for Mexico? Naira for Nigeria?”

- Integrate their API. Most take 2-3 weeks if you already use payment software. 6-8 weeks if you’re on legacy systems.

- Start small. Test one corridor. USD to MXN is the easiest.

- Track savings. You’ll likely cut costs by 50-70%.

Don’t try to build your own liquidity. It’s expensive. Use someone who already has it.

What’s next?

The U.S. Federal Reserve is testing stablecoin integration into FedNow by late 2025. The ECB is launching its own digital euro for wholesale use. This isn’t a fringe experiment anymore. It’s infrastructure.

By 2026, you’ll see:

- More euro, yen, and pound stablecoins approved by regulators

- Bank apps offering “crypto transfer” as a standard option

- Regulators forcing stablecoin issuers to publish daily reserve audits

- More failed payments in underbanked regions-until liquidity providers step in

The goal isn’t to kill banks. It’s to make them irrelevant for the parts of cross-border payments that were broken.

And it’s already working.

Are stablecoin payments legal everywhere?

No. As of 2025, 37 countries have different rules for stablecoins. Some, like Germany and the U.S., have clear frameworks. Others, like Nigeria and Bangladesh, ban them outright. Always check local regulations before sending or receiving payments.

Can I use stablecoins to pay my freelancer in another country?

Yes-if both you and your freelancer use a compatible service. Platforms like BitPay, Coinbase Commerce, or BVNK let businesses send stablecoins directly to wallets. The freelancer then cashes out via their local exchange or payment app. It’s faster and cheaper than PayPal or Wise for international freelancers.

Is USDT safe to use for business payments?

USDT is the most widely used stablecoin, but it’s also the least transparent about its reserves. USDC, backed by Circle and regulated in the U.S., is safer for businesses because it publishes monthly audits. For corporate use, USDC is recommended over USDT.

Why do some crypto payments fail?

Most failures happen at the "off-ramp"-the point where crypto turns into local cash. If the local partner doesn’t have enough liquidity (say, during a market crash), the payment gets stuck. That’s why choosing providers with deep liquidity in your target country matters more than the blockchain you use.

Do I need a crypto wallet to use stablecoin payments?

Not if you’re using a business service. Most platforms handle wallets behind the scenes. You just send money like you would with PayPal. The recipient gets their local currency. You never see crypto. It’s invisible infrastructure.

lori sims

So I just sent $2K to my sister in Mexico last week using USDT through a fintech app-took 7 minutes, cost $18. Compared to Western Union’s $120 and 3-day wait? Absolute game-changer. I didn’t even need to explain crypto to her-she got pesos in her bank account. It felt like magic, honestly. The system just works behind the scenes. No wallet, no keys, no drama. Just money moving like water.

Reggie Fifty

This whole stablecoin thing is just crypto in a suit. You think regulators are gonna let this scale? The Fed’s already drafting rules to strangle it. And don’t get me started on Tether’s reserves-black box with a smile. This isn’t innovation, it’s regulatory arbitrage. We’re trading one opaque system for another. And you call this progress? Pathetic.

Kristi Emens

I appreciate the breakdown, especially the part about liquidity corridors. It’s easy to get swept up in the speed and cost savings, but the real bottleneck isn’t the tech-it’s the money on the other end. If no one’s holding pesos in Mexico or naira in Nigeria, the whole chain breaks. This isn’t just about blockchain-it’s about building real financial partnerships across borders. And that takes time, trust, and capital. Not just code.

Deborah Robinson

My aunt in rural India uses WhatsApp to send money to her brother in Kerala. She doesn’t know what a blockchain is. But when she gets a notification that her payment went through in 5 minutes instead of 3 days? She smiles. That’s the real win. You don’t need to understand the tech. You just need it to work. And for millions, it finally does. Maybe that’s the quiet revolution-not in boardrooms, but in village kitchens.

Michelle Mitchell

so like… stablecoins are just crypto but less risky? but then why do they still crash sometimes? and who even holds the money? like if i send usdt and it turns to pesos… where did the dollars go? this feels like a magic trick where the rabbit is just… gone?

Ryan Burk

37 regulatory frameworks? That’s not a feature-that’s a bug. This isn’t innovation, it’s chaos dressed up in whitepapers. And don’t even get me started on how these platforms are just crypto shell companies with bank licenses. You think Visa or Mastercard are gonna let this eat their lunch? They’re already lobbying to bury this under compliance red tape. This whole thing is a house of cards built on someone else’s liquidity.

Amanda Markwick

I’ve been watching this space for years, and honestly? This is the first time I’ve seen real momentum. Not hype. Not speculation. Actual infrastructure. When banks start saying ‘We’ll use USDT’ instead of ‘We hate crypto,’ you know it’s crossing over. The real win isn’t the 1% fee-it’s the dignity it gives people. No more waiting a week for your kid’s tuition money. No more being scammed by middlemen. This isn’t just faster money-it’s fairer money. And that’s worth fighting for.

Arya Dev

India banned this. And yet, somehow, USDT is everywhere. WhatsApp groups. Telegram bots. Local shopkeepers taking crypto. The government says it’s illegal-but the people? They don’t care. Why? Because the system is broken. The banks are slow. The fees are theft. And now? A 19-year-old in Pune can send money to his cousin in Nairobi faster than the RBI can issue a press release. This isn’t rebellion-it’s evolution. And you can’t stop evolution with a ban.

Andrew Hadder

Just a heads up-if you’re using this for business, make sure your accounting software can track crypto transactions. I got hit with a weird IRS notice because my software flagged ‘USDC deposit’ as ‘unclassified income.’ Took 3 months to fix. You need to document the conversion point. Not hard, but nobody tells you this. And yeah, I typo’d ‘conversion’ above. Oops.

Derek Sasser

For anyone thinking about this for small business: start with USD to MXN. It’s the easiest corridor. Liquidity is deep. Providers are regulated. And the volume is high-so if something goes wrong, support actually responds. Don’t jump into Nigeria or Indonesia yet. The infrastructure isn’t there. And yes, I’ve done this for my freelance design clients. Cut my FX costs by 65%. No joke. It’s real. Just pick a good provider. Don’t go DIY.

Neeti Sharma

USA thinks it’s the center of the world. But in India, we’ve been using UPI for years. Instant, free, under 5 seconds. No crypto needed. Why are we even talking about stablecoins? This is just American tech bros trying to reinvent the wheel. UPI handles 10x more volume than all stablecoins combined. And it’s public. Transparent. Regulated. You’re all chasing ghosts.

Nadia Shalaby

I’m just here to say… I didn’t even know this was a thing until last week. Now I’m sending money to my cousin in Colombia every month. It’s so easy. I just click ‘send’ and boom. Done. No stress. No fees. No waiting. I don’t even think about it anymore. It’s just… normal now. Kinda weird how fast something this big just… showed up.

Fiona Monroe

While the efficiency gains are undeniable, one must not overlook the systemic risks inherent in unregulated liquidity pools. The collapse of a single off-ramp provider-particularly in jurisdictions lacking deposit insurance-poses a material threat to financial stability. Moreover, the absence of a standardized audit framework for stablecoin reserves undermines the very premise of trustless systems. This is not progress; it is regulatory arbitrage masquerading as innovation.

Molley Spencer

Let’s be real: stablecoin payments are just the latest financial engineering gimmick for hedge funds to move capital without reporting. The ‘$19 trillion’ figure? That’s mostly wash trading between Binance, OKX, and Kraken wallets. The real cross-border volume? Maybe 20% of that. And don’t even get me started on the tax evasion potential. This isn’t revolution-it’s a laundering pipeline with better UX. And yes, I’ve seen the spreadsheets. The numbers don’t add up. The rest of you are just drinking the Kool-Aid.